It’s been a year since the market bottomed out during the COVID-19 sell-off. The 33.8% drop in the S&P 500 brought to a sudden end one of the longest bull markets in history. But as the dust has settled and the markets have returned to all-time highs, many people were left wondering: was that really a bear market?

On one hand, the COVID sell-off met the strict definition of a bear market, that is, losses in excess of 20%. On the other hand, the suddenness of the sell-off and the rapidity of the recovery has led to a counter argument, that this was more of an extreme correction rather than a true bear market.

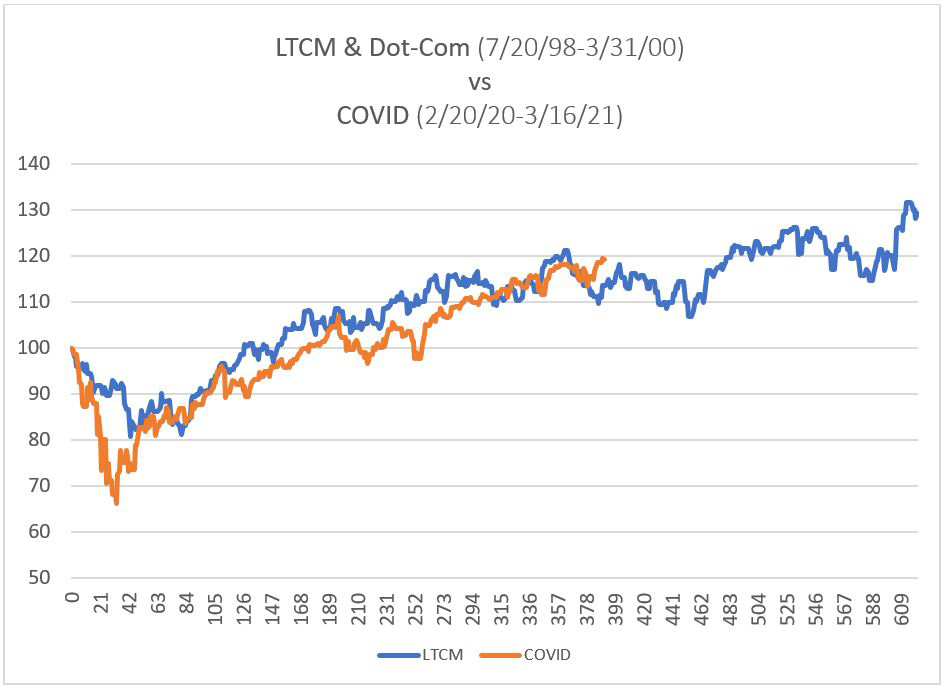

The massive COVID-19 sell-off and subsequent rebound of 2020 was unprecedented:

That said, if I were to look for a historical comparison, I would find the closest parallel in the 1998-99 period.

Source: Morningstar Direct

Beyond the numbers, there are other parallels between 1998/99 and 2020/21:

This late-90’s period was known at the time of “Irrational Exuberance.” Although then-Fed Chairman Alan Greenspan first used the phrase in December 1996, the bubble continued to form for several more years, brushing off the near-miss bear market of August 1998.

Students of history know what happens next: the long bear market of 2000-2002.

While the Dot-com bubble burst in March 2000, this period was marked by other calamities and challenges. The terrorist attacks of September 11th and the accounting scandals of Enron, Tyco, and WorldCom led to an extended drawdown. The S&P 500 drew down by almost 45% and did not recover its losses until October 2006. Meanwhile, the NASDAQ lost nearly three-quarters of its value and did not fully recover until December 2013, almost a decade and a half later.

That was a true bear market.

While there are many similarities between the 1999 period and today, there is one large difference. The markets entered the new millennium with yields at comfortable levels. The 10-year Treasury was around 6.5% on January 1st, 2000. This had several benefits to diversified investors:

Today, in stark contrast to the 2000’s, yields on the U.S. 10 year Treasury Note are a paltry 1.6%. It is highly unlikely bonds will be able to provide those levels of positive returns should we face a true bear market again.

Investors currently find themselves faced with unpleasant realities and challenges. Some are familiar, as the equity market today resembles that of the Irrational Exuberance period. Other challenges are new, like the doubt surrounding bonds being able to perform their traditional protection role.

Swan believes that this widespread uncertainty requires new thinking. Our “always invested, always hedged” approach was designed to navigate such treacherous waters. In fact, Randy Swan created the Defined Risk Strategy all the way back in 1997, when his concerns about market valuations and irrational exuberance led him to create a hedged equity strategy that would hedge the gains he made in the bull market.

Today many investors face a similar conundrum: how does one participate in equity markets gains, yet defend against potential losses? We believe that hedged equity as a strategic investment approach is more relevant than ever.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Marc Odo, CFA, FRM, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. Formerly, Marc was the Director of Research for 11 years at Zephyr Associates.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap-weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities that vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives.

All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. All investment strategies have the potential for profit or loss. Further information is available upon request by contacting the company directly at 970-382-8901 or swanglobalinvestments.com.com. 071-SGI-032621