The Villains of 2022’s Horror Show

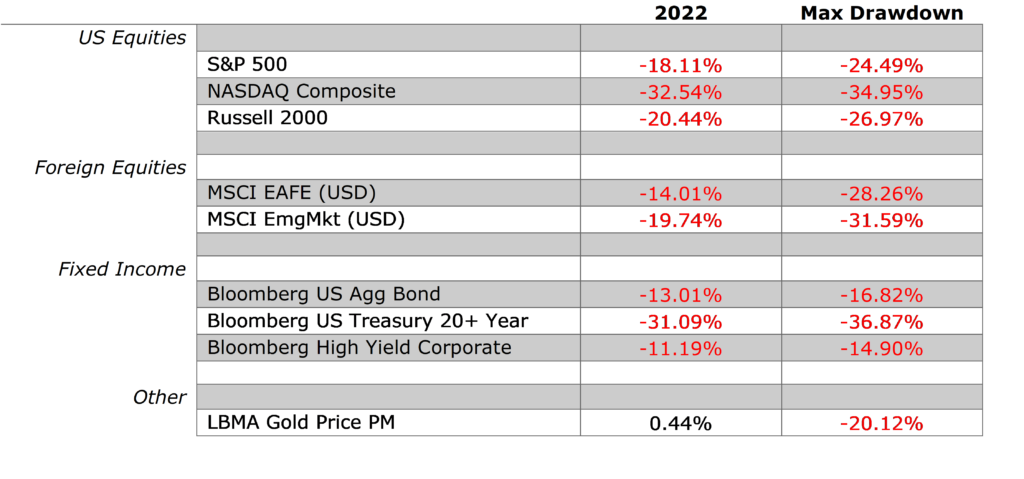

There’s no denying that 2022 was a grueling year for investors. It seems like everyone lost money, regardless of the investment strategy or asset class.

Source: Morningstar Direct

The standard explanation for this sorry state of affairs is always the same- inflation and rising interest rates. Is it really possible that these twin villains are to blame for losses across so many different asset classes? In this blog post we will dig deeper and explain just how inflation and rising interest rates negatively impacted so many different investments around the globe.

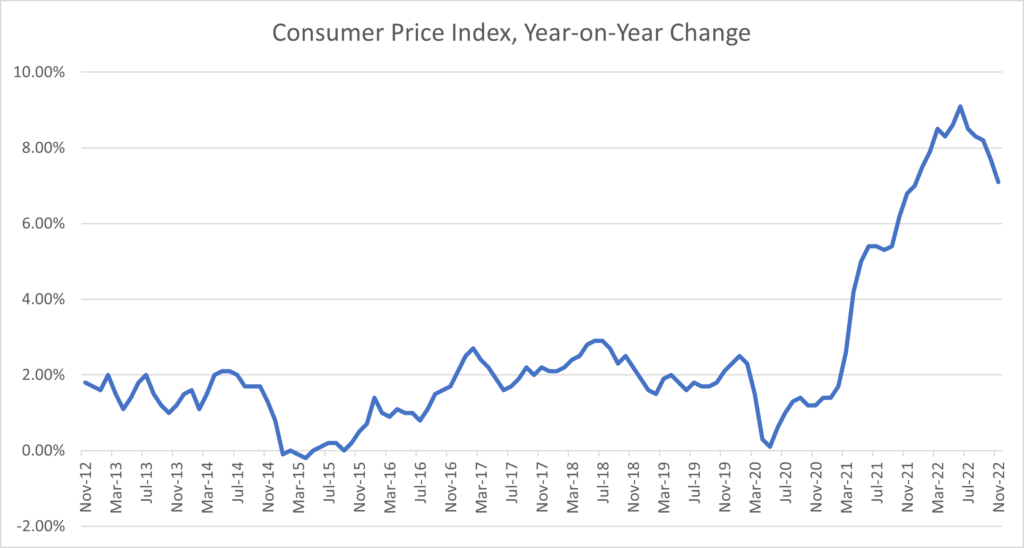

Source: U.S. Bureau of Labor Statistics.

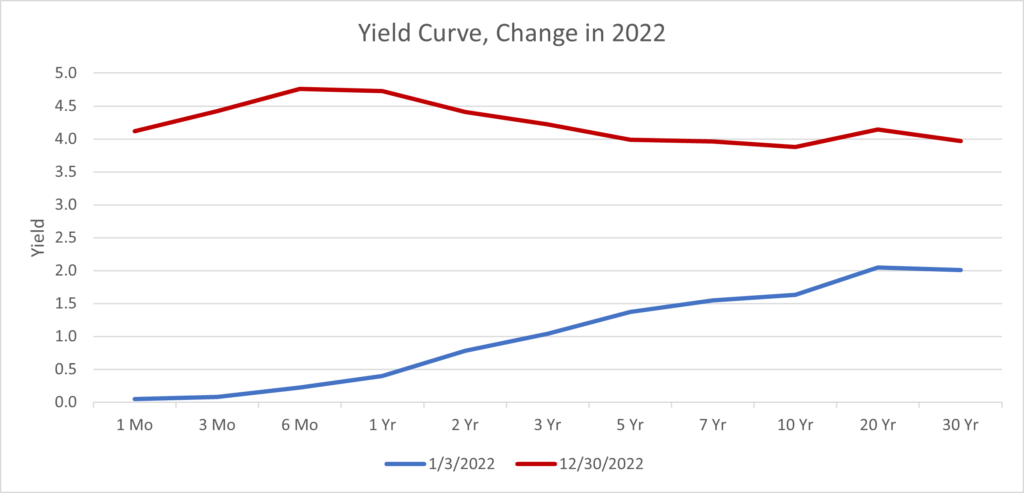

Source: U.S. Department of the Treasury

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

We will start with the big picture. Ever since the turn of the century, the Federal Reserve’s solution to any problem was loose monetary policy. Whether it was the Dot-Com Bust (2000-02), the Global Financial Crisis (2007-09) or the COVID-19 Pandemic (2020), the standard response was to flood the economy with liquidity.

Classically educated economists warned that such a state of affairs could not be maintained indefinitely without unleashing the scourge of inflation. The tipping point came after the COVID-19 Pandemic, when loose monetary policy was coupled with extremely generous fiscal stimulus. Much to the chagrin of starry-eyed proponents of “Modern Monetary Theory”, the harsh reality is you can’t endlessly print money without it negatively impacting prices and labor markets.

Although the response was belated, the Fed is now taking the risk of inflation seriously. While not as extreme as Paul Volcker’s inflation-busting campaign of the early 1980’s, the remedy is the same: to vanquish inflation, the Fed is intentionally cooling down the economy by tightening monetary policy. It is an unenviable choice, but the Fed has determined that slowing the economy is the lesser of two evils.

The problem with such an approach is that it takes a fair amount of time for rate hikes to impact the broad economy. During that time the Fed runs the risk of overshooting its target. The goal is to slow down the economy, not cause a recession. But given the lag in both price effects and economic activity, there is a real risk that the Fed’s rate hikes tip the economy into an outright recession.

The U.S. stock market, as measured by the S&P 500, was underwater for almost the entire year and dipped into bear market territory several times. It is often said that stock markets are forward-looking. If that’s the case, that means today’s investors are forecasting a cloudy future. There are several ways in which high inflation and rising interest rates negatively impact stocks.

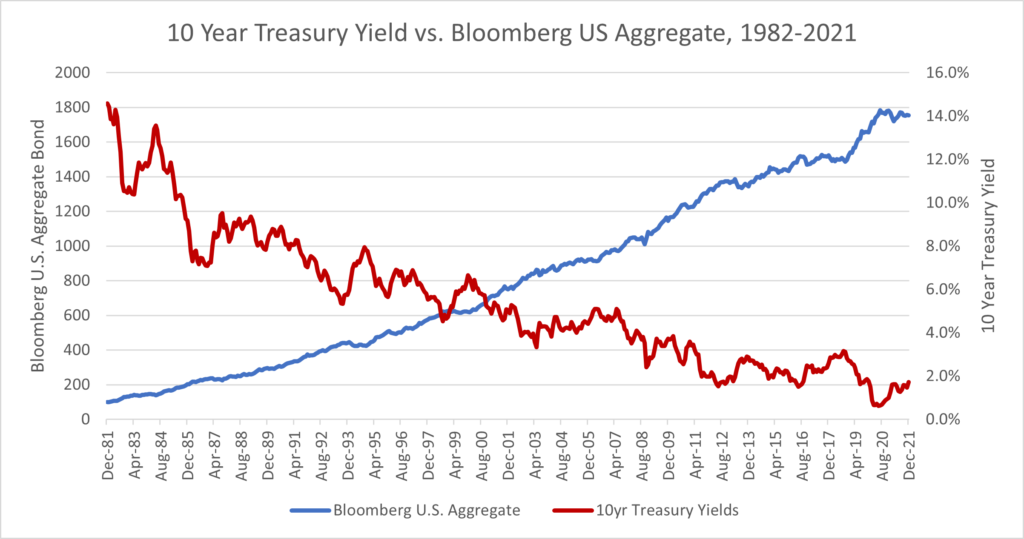

Bonds have also been a casualty of rising interest rates. Ever since rates retreated from their double-digit levels in the early 1980’s, bonds have had the wind at their backs. Bondholders were able to have the best of both worlds- income exceeding inflation and capital preservation when equity markets sold off. The Bloomberg U.S. Aggregate Bond index had an average annual return of 7.42% from 1982 to 2021.

Source: St. Louis Fed, Zephyr StyleADVISOR

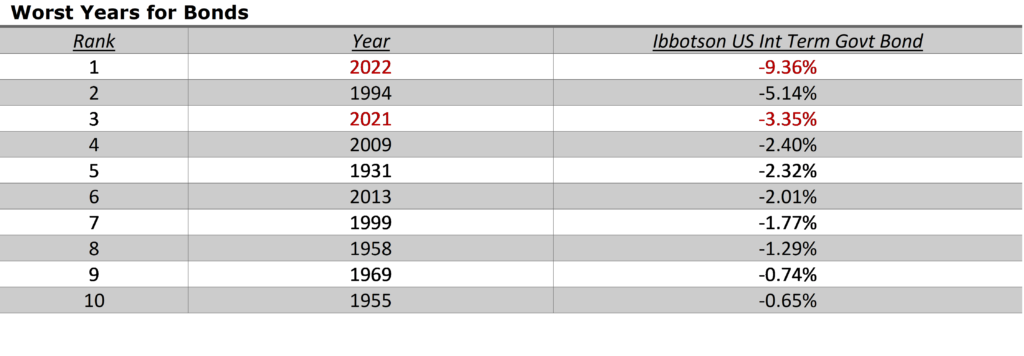

Now that dynamic has reversed and the rate environment is a headwind rather than a tailwind. In 2022 the Ibbotson US Intermediate Term Government Bond index had its worst year since the index’s inception in 1926. The third-worst year on this list was the prior year, 2021, as the threat of rising rates started to impact bonds.

Source: Morningstar Direct

Inflation and rising rates negatively impact bonds in a number of ways.

Collectively these factors are known as duration risk. Professional bond managers are aware of duration risk. However, for the average bond holder who viewed bonds as the “safe” portion of their portfolio, duration risk has come as a nasty surprise.

High yield or non-investment grade bonds are doubly impacted by the current situation. In addition to all the duration/rising interest rate risks mentioned in the previous section, high yield bonds are subject to credit risk.

During the era of low interest rates, it made sense for companies to refinance or leverage up given the fact that debt was so cheap. However, those salad days are over and if companies need to rollover that debt, it will be at much higher levels. Moreover, companies that issue non-investment grade debt are assumed to be in a more precarious financial position and would be more challenged in a recessionary environment. This does not bode well for high yield debt.

Granted, there is a lot of variability across sectors and individual companies. Some companies have healthier balance sheets and will likely be able to weather a storm. A lot of high yield bonds were issued with liberal covenants, giving them more operational leeway. We explore the risks in high yield in more depth here.

However, as Warren Buffet famously said, “Only when the tide goes out do you discover who’s been swimming naked.” An economic slowdown might expose those companies at risk of default or bankruptcy.

Increases in U.S. interest rates makes U.S. based investments, and thus the U.S. dollar, relatively more attractive to global investors. The U.S. dollar had remarkable strength versus the Japanese yen, British pound, and Euro in 2022. However, dollar strength is not necessarily a good thing. The dollar trading near record highs has had some negative effects, including:

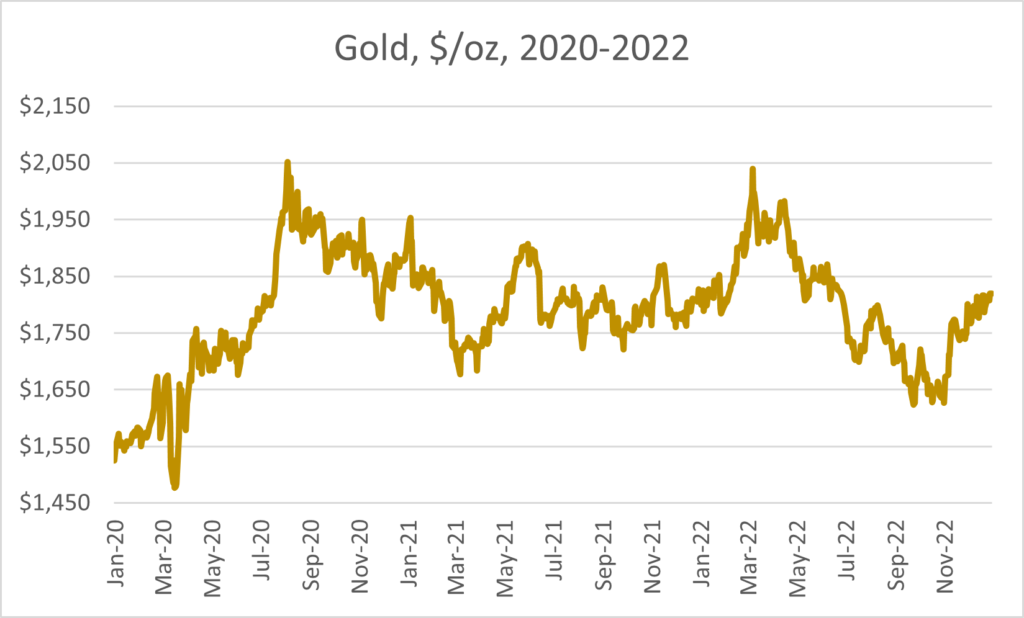

Gold has traditionally been thought of as a store of value during difficult times and as a hedge on inflation. If that’s the case, why didn’t gold do better in 2022? With capital markets down and inflation skyrocketing, why is gold suffering? The answer is two-fold.

First, gold did enjoy a healthy run-up during the Covid-19 pandemic. Between January 1st, 2020 and August 5, 2020, gold went from $1,524 to $2,051, an increase of 34.5%. Early movers into gold did make money, but then some investors rotated out and took profits.

Source: finance.yahoo.com

The more recent factor driving the price of gold down is the opportunity costs of holding gold. One of the traditional negatives of gold is that gold has no cash flow. Gold pays no yield. As long as bond yields were close to zero, this factor was moot. However, with 10-year Treasury bonds now yielding around 4%, anyone parking their money in gold must be willing to forgo the “risk free” opportunity cost of a nearly 4% Treasury yield. On a relative basis, gold is less attractive than it was when bond yields were near zero.

The above chart clearly illustrates this relationship. The recent high point for gold occurred on March 8th at $2,040/oz. The this is right around the time that the Fed started raising rates. Since then, the price of gold has moved in the opposite direction of rising rates.

One might hope that with the Fed raising short-term lending rates, an immediate beneficiary would be rates on CDs and savings accounts. Long-suffering savers, stuck with 0% interest rates, should logically see an improvement in yields, right?

Unfortunately, that hasn’t been the case. The big banks are in no hurry to increase their interest rate costs by offering rates more in-line with their lending rates. The official explanation is that the banks have more than enough deposits on hand to fund their lending needs. It would appear that interest rates in savings accounts quickly respond to cuts in Fed rates but are sticky when it comes to increases- the worst of both worlds for savers.

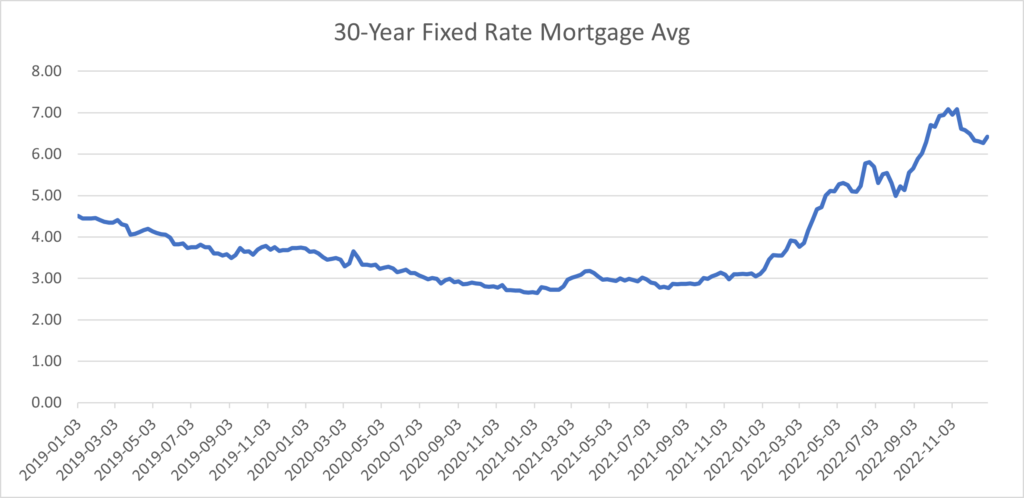

The line between rising interest rates and a drop-off in house prices is a straight one. In less than a year the rate on a 30-year mortgage went from under 3% to over 7%, one of the largest and fastest rises in history.

Source: St. Louis Fed

This casts a pall over the housing market. Potential buyers can no longer afford monthly payments at these higher rates. Sellers are unwilling to mark their house prices down to reflect the new reality. Borrowers with floating-rate mortgages will see steep increases in their monthly payments. Current homeowners who might have considered tapping their home equity or purchasing a new upgraded home are reluctant to swap out their old low-rate mortgages for new high-rate loans.

For many families, a house is their largest store of value, dwarfing capital market investments. The global value of housing is $250 trillion, compared to the aggregate value of equity markets of $90 trillion[1]. While it seems unlikely that housing will become a systemic crisis like it was in 2007-09, a depression in housing prices could be a long-term drag on the economy.

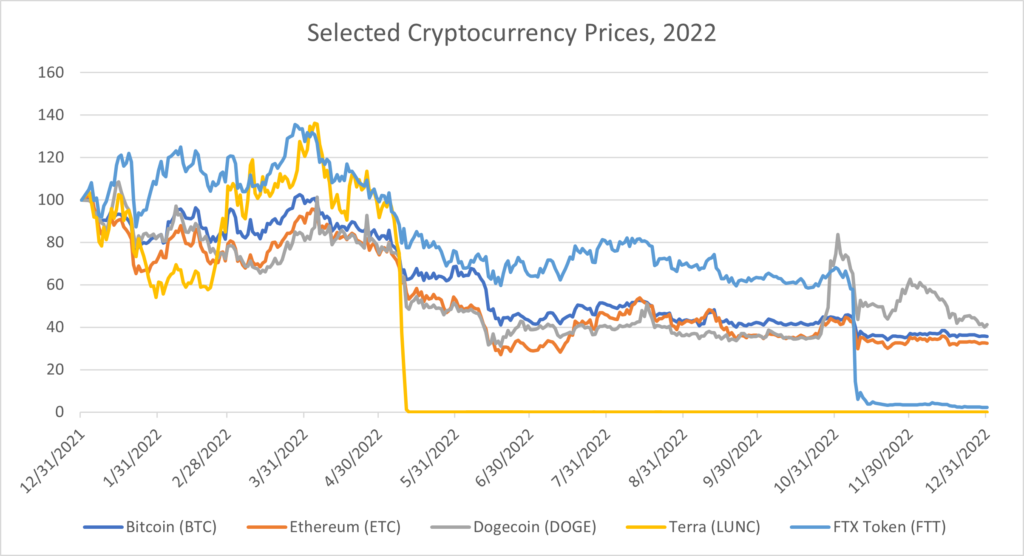

Leading up to 2022, there was a ridiculous amount of hype surrounding “get rich quick” investments like cryptocurrencies, non-fungible tokens (NFTs), special purpose acquisition companies (SPACs), collectibles, and “meme” stocks. These schemes are more akin to gambling than investing and have been in freefall over the last year.

While these various moonshots might seem like they have little in common, one can argue they are all simply examples of too much money chasing too few good ideas. The trillions of dollars that flooded the economy during Covid-19 pandemic helped inflate these bubbles. While certainly some money was used as intended- to replace lost wages or help with living expenses as the economy went into shock- a lot of it chased spectacular returns in speculative investments. Now that the “free money” taps have been turned off the case for these moonshots is much harder to make.

Source: finance.yahoo.com. Prices scaled to 100 on 12/31/2021

For those market participants with a grasp of history, this is just the latest example of “irrational exuberance” fueling a speculative bubble. Those who “invested” at the peak of the hype-cycle will likely get pennies on the dollar, if anything, as a return. The bigger, more important question going forward is whether or not these losses will be contained to the punters or if there are spillover risks to the broader economy.

It might seem overly simplistic to pin all of 2022’s woes on the common factors of inflation and rising interest rates. Hopefully this paper illustrated that yes, the end of loose monetary policy is the smoking gun responsible for the poor performance of equities, bonds, gold, the housing market, and the moonshots.

The “everything bull market” that followed the Global Financial Crisis was a one-legged stool, supported by easy money. The central banks kept the party going as long as they possibly could, but eventually the punch bowl had to be taken away. Now investors are dealing with the hangover.

Traditional portfolio construction relies on traditional asset classes to provide blended sources of return and risk mitigation through diversification. 2022 was a horror show for traditional asset classes- with nearly all suffering losses at the same time. To the extent that elevated levels of inflation persist and/or that interest rates continue higher, returns for traditional asset classes may continue to disappoint investors.

Rising inflation and interest rates were the villains in 2022. It is a form of market-wide risk that cannot be diversified away. However, market risk can be hedged. Hedging market risk can be accomplished by using put options, which are inversely correlated to the underlying investment, that may provide investors true diversification in what seems like an “everything bear market.”

Options-based, hedged equity strategies offer investors a way to remain invested in the equity market, while maintaining a hedge for risk mitigation position. This approach doesn’t rely on bonds, with their high sensitivity to rising interest rates. Such strategies may provide a way for investors to navigate the risks of elevated or sticky inflation and the impacts of future interest rate hikes that may persist into 2023 and beyond.

Marc Odo, CFA®, FRM®, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. His responsibilities also include producing most of Swan’s thought leadership content. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 003-SGI-010923

1A bear market is technically defined as a loss of 20% or more.

Swan Global Investments is an SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (DRS). Please note that registration of the Advisor does not imply a certain level of skill or training. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be no assurance that future performance will be comparable to past performance. This communication is informational only and is not a solicitation or investment advice. Further information may be obtained by contacting the company directly at 970-382-8901

or www.swanglobalinvestments.com. ***-SGI-02**22