This site uses cookies. By continuing to browse the site, you are agreeing to our use of cookies. Privacy Policy

Okay, thanks

It seems like everything has changed over the last year. The standard 60% equity, 40% bond model that worked so well for decades is down 16.6% through October 31st. The security blanket of “the Fed put” bailing out investors is nowhere to be seen. Inflation, long dormant, has surged to be the number one concern for many in America and across the globe. Cryptocurrency and other “moonshots” that made billionaires out of thin air are rapidly evaporating.

With so much changing so quickly, it is worth asking, “Has anything remained the same?” In our opinion, there is one truth that has endured through 2022’s carnage:

“You can’t fight the Fed.”

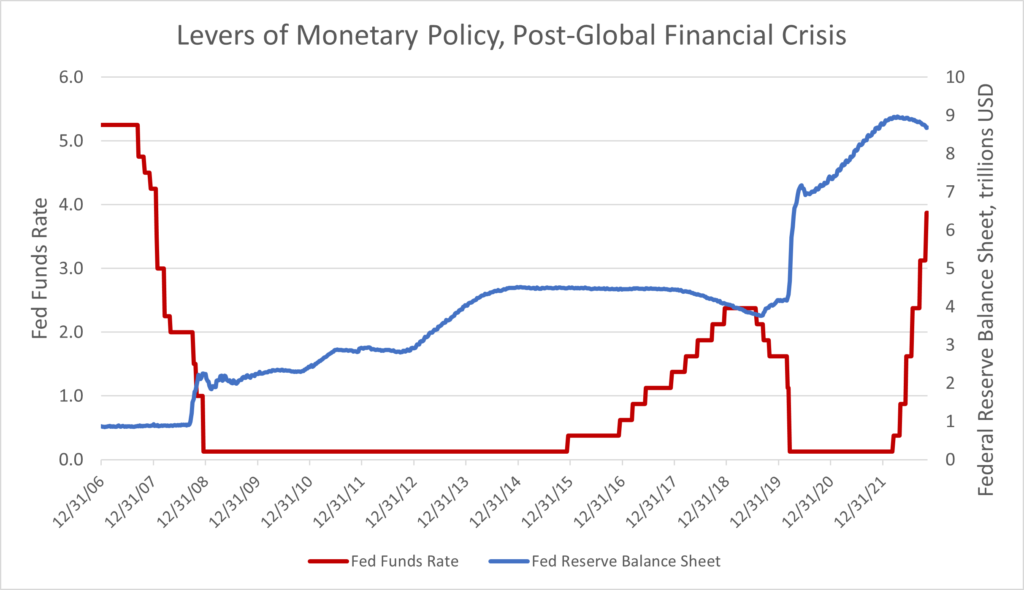

Since the turn of the century, the Federal Reserve’s answer to any problem was loose monetary policy. Sometimes the calamities were quite large and warranted a robust policy response- think of the Dot-Com Bust & September 11th attacks (2000-02), the Global Financial Crisis (2007-09), and the Covid-19 Pandemic (2020). Other times, like the Taper Tantrum (2013) or the near-miss bear market in the fourth quarter of 2018, there was weak justification for continued loose monetary policy. But the Fed proceeded anyway.

There’s an old saying: “to a hammer, everything looks like a nail.” In this case, the Fed’s monetary policy was the hammer, and its answer to any problem was to keep money cheap and flowing.

Source: St. Louis Fed

This flood of liquidity lead to what people would call “the everything bull market.” It seemed impossible not to make money, as major investable asset classes reached record highs.

Level-headed investors raised warning flags, but in vain. Surely future earnings couldn’t possibly support current equity prices? Lenders weren’t actually paying borrowers to take their money, right? Certainly anyone who knew about tulip bulbs and the South Sea Bubble saw disturbing parallels in collectibles and SPACs, didn’t they?

You can’t fight the Fed. As long as the money machine was printing, prices continued to defy gravity.

Until, of course, it stopped.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

The Fed was finally forced to reverse course after inflation rocketed to levels not seen since the early 1980’s. Given the choice between continued high inflation and the risk of instigating a recession, the Fed has clearly picked its poison. The Fed has embarked on a sustained campaign to tighten monetary conditions. The Fed Funds rate has gone from 0.00%-0.25% to 3.75%-4.00% in 2022, often taking the form of 75 basis point moves. The rate on 10-year Treasuries has gone from 1.52% at the end of 2021 to 4.10% on October 31st. Quantitative easing has ended as the Fed seeks to pare down its bloated balance sheet.

As a result, the “everything bull market” has turned to the “everything bear market.” Equities, bonds, and real assets are all down significantly. The moonshot gambles aren’t just down, they’re imploding.

|

|

|

Through 10/31/22 |

|

Through 12/31/21, annualized |

||

|

YTD |

1 year |

5 years |

10 years |

|||

|

Equities |

||||||

|

S&P 500 |

-17.70% |

28.71% |

18.47% |

16.55% |

||

|

Russell 2000 |

-16.86% |

14.82% |

12.02% |

13.23% |

||

|

MSCI EAFE Index |

-22.81% |

11.78% |

10.07% |

8.53% |

||

|

Bonds |

||||||

|

Bloomberg U.S. Aggregate |

-15.72% |

-1.54% |

3.57% |

2.90% |

||

|

Bloomberg U.S. Corp High Yield |

-12.53% |

5.28% |

6.30% |

6.83% |

||

|

Real Assets |

||||||

|

Gold London PM Fixing |

-9.95% |

-3.75% |

9.70% |

1.75% |

||

|

Case Shiller US National Houses |

N/A |

19.25% |

8.84% |

7.33% |

||

|

Alternatives |

||||||

|

Bitcoin |

-56.82% |

16.21% |

108.77% |

N/A |

||

|

Ethereum |

-53.81% |

104.43% |

201.85% |

N/A |

||

Sources: Zephyr StyleADVISOR, finance.yahoo.com, Federal Reserve Economic Data. Case Shiller data operates with a three-month lag and is unavailable through 10/31/22

One could look at each of these asset classes individually and argue over the pros and cons of each. However, if one takes a step back and looks at the forest rather than the trees, the case can be made that one factor is driving all these assets down. The end of loose monetary policy is the one thing that negatively impacts all these asset classes.

Modern portfolio theory was always based on the premise that low correlations between the constituents of a portfolio would lead to lower overall portfolio volatility. Mathematically, this can be proven true. However, that promise of lower volatility is contingent on low or negative correlations. If, on the other hand, all the constituents of a portfolio share a high correlation to a common factor, then diversification will fail to significantly reduce risk- creating a correlation conundrum.

Rising interest rates is that common factor in this nightmare scenario. It is a form of market-wide risk that cannot be diversified away. However, market risk can be hedged. Hedging market risk can be accomplished by using put options, which are inversely correlated to the underlying investment, that may provide investors true diversification in what seems like an “everything bear market.”

Options-based, hedged equity strategies offer investors a way to remain invested in the equity market, while maintaining a hedge for risk mitigation position. This approach doesn’t rely on bonds, with their high sensitivity to rising interest rates. Such strategies may provide a way for investors to navigate the Fed’s new course of tighter monetary action instead of fighting a losing battle.

Marc Odo, CFA®, FRM®, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. His responsibilities also include producing most of Swan’s thought leadership content. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 323-SGI-112122