This site uses cookies. By continuing to browse the site, you are agreeing to our use of cookies. Privacy Policy

Okay, thanksMay, 10, 2023

Bank Failures 2023 & The Dangers Still Lurking Beneath the Surface

It’s been said that the road to Hell is paved with good intentions. The difficult situation that many mid-size, regional banks currently find themselves in is a direct consequence of policy decisions made over the last 15 years. While the intentions behind these policies were well-meaning, the consequences of these decisions have been dire.

2023 has seen the biggest bank failures since the Global Financial Crisis of 2007-09. The current banking emergency has claimed Silicon Valley Bank, Signature Bank, and now First Republic Bank. Market watchers are wondering if there are more dominoes set to fall. The tragedy of the situation is that these consequences were entirely foreseeable if one simply maintained a skeptic’s outlook and asked the right questions.

Hoping to prevent further calamities, different policy solutions are being proposed to limit the risk of further bank failures. While well-meaning, these “solutions” will have consequences of their own. Swan only asks that readers consider the consequences.

So how did we get here?

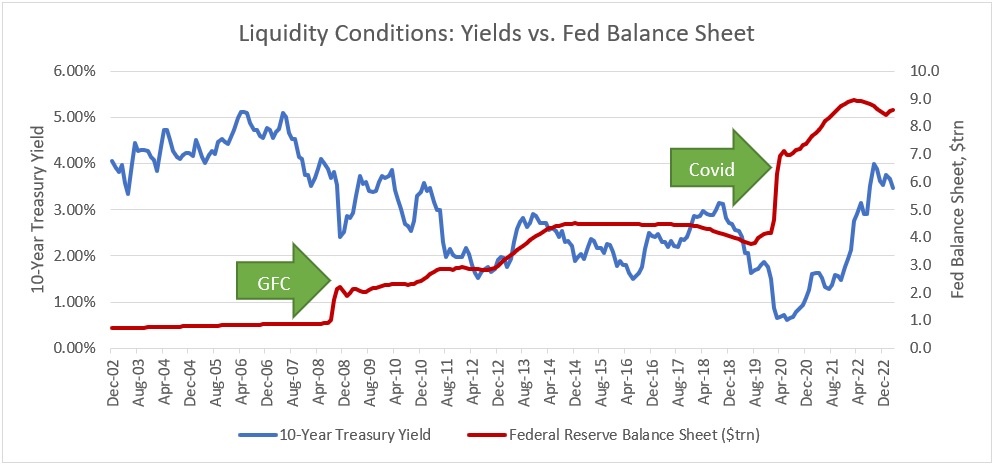

In Swan’s estimation, the Original Sin of this story was one exceptionally loose monetary policy. Following the Global Financial Crisis of 2007-09, money was kept far too cheap for far too long, which has led us to this current predicament.

While one could make the argument that emergency measures were required to prevent a full-on, systemic collapse of the global financial system, it is much harder to defend the idea that liquidity conditions should have been kept so loose throughout the 2010’s.

The intent of this prolonged period of liquidity was to “keep the good times” rolling. Any time that the markets responded negatively to a tightening in the money supply, like the Taper Tantrum of 2013 or the near-miss bear market at the end of 2018, the Fed quickly lost its nerve and turned the monetary spigots back on.

The consequence of this decision was the issuance of trillions of dollars of debt offering only the sparsest yields.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Source: St. Louis Fed, Economic Research Division

The next calamity to have long-reaching consequences was the Covid-19 pandemic. Faced with a global economic shut-down, authorities responded with a firehose of monetary and fiscal stimulus.

Again, the intention of the efforts was noble- to keep citizens from falling into destitution. But the consequence of trillions of dollars pumped into the economy was the highest inflation in 40 years. A more sober-minded analyst would have predicted such an outcome, but amid a crisis such cautionary voices were drowned out.

Source: Zephyr StyleADVISOR

Once inflation became too big to ignore the Federal Reserve Bank belatedly started draining liquidity from the system. The Fed rapidly raised interest rates and started whittling down their vast balance sheet. After all, price stability is one of the official objectives of the Federal Reserve; supporting the stock market is not.

Once again, the intent was good, but the consequences were dire. Inflation needed to be brought down as it damages broad swaths of the economy and the citizenry. However, the consequence of the rate hikes was to drive down the value of many financial assets. In a world where inflation was approaching 10% and yields were back above 5%, one of the most susceptible assets to rising interest rates is long-term, low-yielding bonds.

Throughout 2022 investors saw the impact of rising rates on both their equity and bond holdings. The S&P 500 index returned -18.1% and the Bloomberg U.S. Aggregate Bond index had its worst year in history with a -13.0% return.

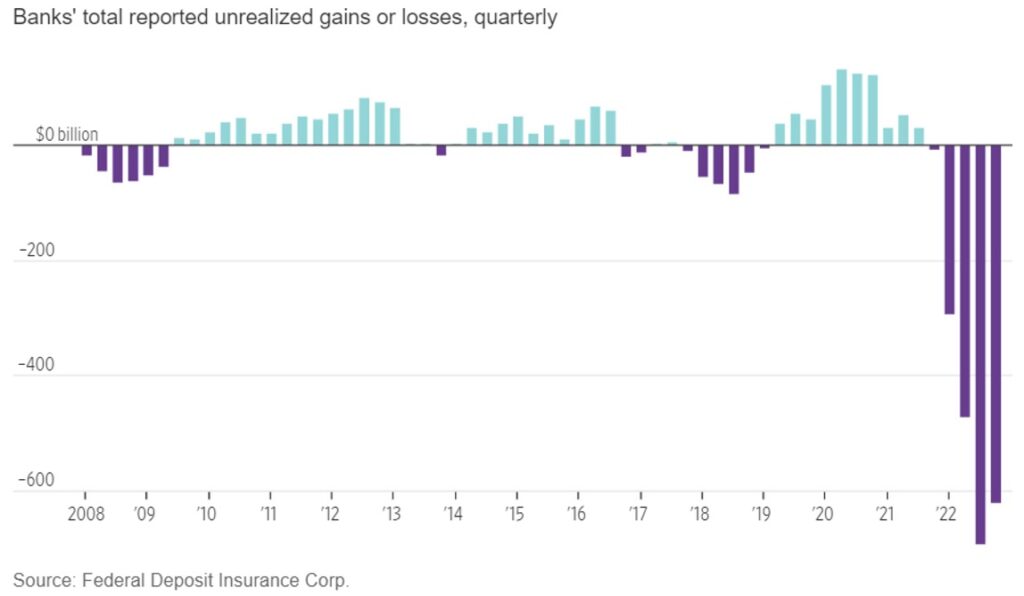

Hidden from view was the impact of these rate rises on the bond and loan holdings of banks. Investors in fixed income bond funds would see their holdings marked-to-market on a daily basis; the pain was immediate and visible. However, depending on the size of the bank and how the bonds were classified, regional banks were able to defer the problem and weren’t forced to immediately recognize the problem. But that doesn’t mean the problem wasn’t there.

Once again, we turn to intentions and consequences. In 2018 the regulations were relaxed for smaller banks. Previously every bank with assets greater than $50 billion was required to undergo Federal Reserve stress tests to gauge the impact of adverse scenarios, as well as meet stricter capital requirements. By changing the requirements from $50bn to $250bn the intent was to relieve some of the regulatory burden and costs from regional lenders- certainly a reasonable goal. However, by reducing the oversight in banks in the mid-size range, these festering problems were overlooked for most of 2022.

The above graph illustrates the unrealized bond losses on bank portfolios. If the bonds are classified as being “held to maturity”, the losses needn’t be recognized. However, if circumstances dictate that these bonds are sold the price will be whatever the market deems fair, and these losses could be realized.

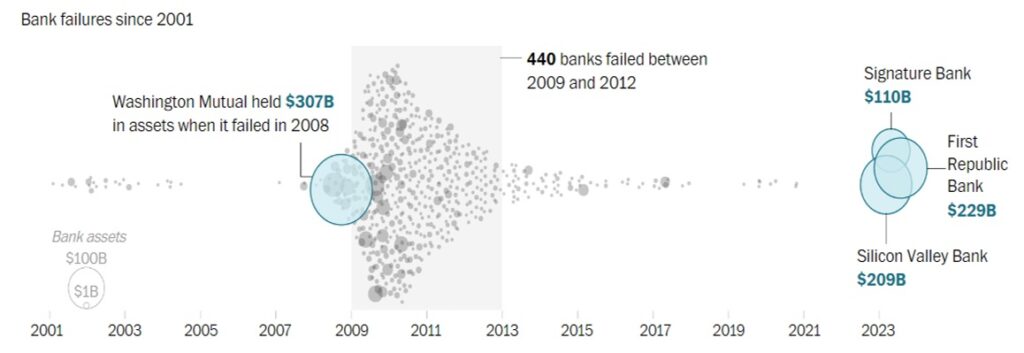

In early March Silicon Valley Bank and Signature Bank experienced a 21st-century bank run, where skittish depositors started moving uninsured deposits out of these troubled banks. Unable to raise capital or stem the outflow of deposits, these banks collapsed and the Federal Reserve stepped in and took over their operations. A month later, First Republic was forced into the arms of JP Morgan Chase. These three failures are the second-, third-, and fourth-largest bank failures in U.S. history.

Source: The Washington Post, “Three of the Four Largest-Ever Bank Failures Have Happened Since March”, May 1, 2023

Although the Federal Deposit Insurance Corporation (FDIC) insures deposits up to $250,000, a large portion of the deposit base of those failed banks were commercial deposits or those of high net-worth individuals, exceeding the FDIC protection limit. Any individual or company worried about the safety of their deposits would want to withdraw their money while they still could. However, the consequence of this rational response is a panic; collectively the actions of many depositors pulling their funds creates a bank run. Forced to meet an avalanche of withdrawals, these troubled banks had no choice but to sell their devalued bonds on the open market, and the unrealized losses become realized.

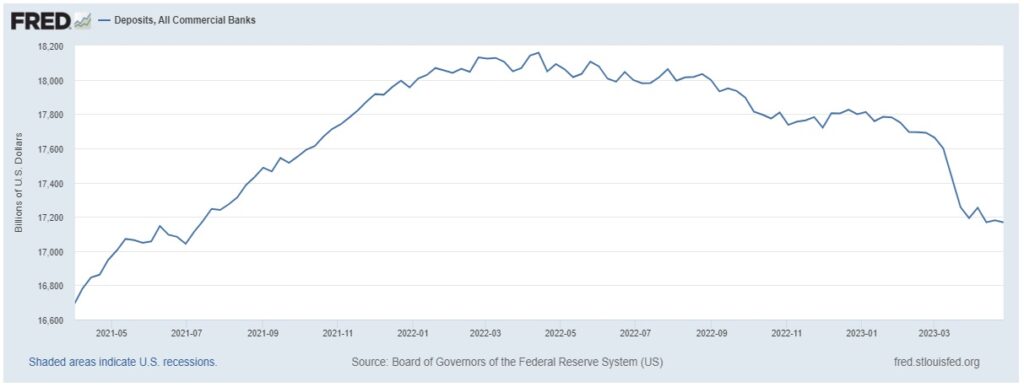

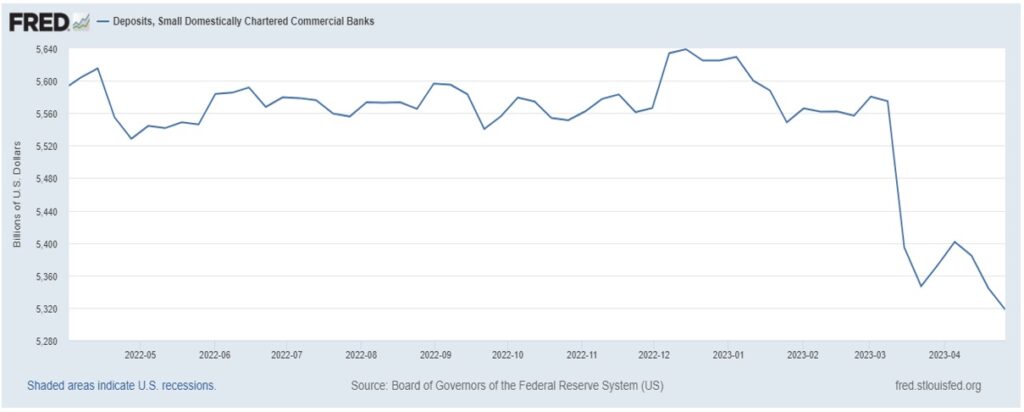

Those who are hoping the worst of the current banking emergency is behind us point to the unique make-up of those failed banks’ depositor base. Highly concentrated and top-heavy in uninsured accounts, these banks were very susceptible to a bank run. However, looking across the broad spectrum of banks, trends are pointing to a broad decline in deposits across the banking system.

Source: St. Louis Fed

There are multiple reasons for these outflows. Some savers are chasing higher yields offered by money market funds or CDs. Some consumers are running down the cash buffers they built up during the pandemic. Others are fleeing the smaller, regional banks for the relative safety of large institutions like Chase or Bank of America.

Regardless of the reason, the consequence of deposit flight is pressure on the smaller, regional banks to:

None of these options are attractive to the management or shareholders of these banks.

With investors nervously waiting for the next domino to fall and short-sellers licking their chops, the question shifts to “Where do we go from here?” In this section, we will discuss several well-intended solutions, but we will also discuss the potential consequences.

Some politicians are seizing the opportunity to grandstand and are demanding a return to stricter regulatory oversight, which might include higher capital ratios, more stringent stress tests, and/or the quicker recognition of losses. While those ideas might have prevented us from getting into this mess in the first place, it is unclear whether they will be helpful getting us out. Again, returning to the theme of “beware of unintended consequences”, these politicians should ask themselves if the situation would really be improved if, all of a sudden, dozens of regional and community banks were forced to raise capital or start realizing duration-related losses. If anything, these “solutions” might lead to further panics and make the problems worse, not better.

There are also the unintended consequences of further consolidation within the industry. The only banks large enough to acquire banks like First Republic are the behemoths like JPMorgan Chase, Bank of America, and Wells Fargo. Given the “too big to fail” scorn that politicians love to heap upon these giant financial firms, do they really want to implement solutions that only make them bigger?

Even if tightening regulatory standards doesn’t lead to further bank runs, other unintended consequences should be considered. Market forces are already leading banks to tighten their lending standards. Commercial and real estate loans have been harder to come by and more costly as banks brace for an economic slowdown or even a full-blown recession. Do regulators want to further handcuff regional banks by tightening the rules when the economy is on the brink of a “hard landing?”

Unfortunately, the alternatives don’t look much better. Even if the banks aren’t forced to raise capital or realize their losses, a big portfolio of low-yielding loans and bonds might be an albatross around the neck of lending for quite some time. Banks might wait for their loans and bonds to mature, which could take years or even decades. They might hope that the Fed starts cutting rates and they could claw back some of the unrealized duration losses. However, the consequence of such inaction is the “zombie bank” problem, where banks unprofitably stagger along and refrain from lending. By failing to lend and provide capital, banks would be failing in their primary purpose.

A third alternative to the “more regulation” and “no changes” paths described above would be a “less regulation” solution. While there aren’t too many voices calling for further liberalization of the rules, another path would be to loosen the rules and allow banks to invest more aggressively with the intent of outgrowing their problems.

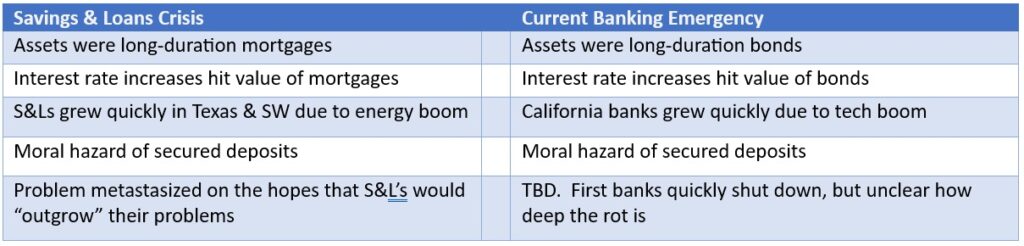

Once again, unintended consequences should be considered. Given the “moral hazard” of deposit insurance, decision-makers at banks are incentivized to take high risks: if the investments work out the bank benefits, but if the bets don’t pay off the government steps in and picks up the bill. If those investments go wrong, the problem will be made worse, not better. The reason why the “less regulation” solution isn’t receiving too much consideration is the consequences were pretty dire the last time it was tried- i.e. during the Savings and Loans Crisis of the 1980’s.

The closest historical parallel to the current banking emergency is not the Global Financial Crisis of 2007-09. The Global Financial Crisis was more like a Jenga tower collapsing. With every brick that was removed the Jenga tower became wobblier, until the whole edifice tumbled down when the key brick, Lehman Brothers, was removed.

Swan believes that the Savings and Loans Crisis of the 1980’s is a more fitting comparison.

After inflation skyrocketed to double digits in the late 1970’s and early 80’s, Fed Chairman Paul Volker implemented a brutal but effective series of interest rate hikes that brought inflation under control. While certainly a victory, there was undeniably a cost. The economy was pushed into a recession in the early 80’s and the banking industry was hit hard.

Savings & Loans Banks, or “thrifts”, were established with the primary objective of lending residential mortgages. The regulations were strict; S&Ls couldn’t operate across state lines and initially couldn’t lend much to other sectors of the economy. Moreover, the idea of securitizing mortgages and moving them off the S&L’s books was many years in the future. Savings and Loans were stuck holding long-duration assets at a fixed rate.

Volker’s inflation-busting interest rate increases blew up this model. Loans made in a low-rate environment were worth much less when the prevailing rate on 30-year Treasuries ballooned to over 15%. Moreover, S&L’s couldn’t offer competitive depositor rates and handing out free toaster ovens wasn’t going to keep deposits in-house.

Faced with this brewing crisis, the authorities made a fateful decision; one with disastrous consequences. Rather than deal with the problem in its early stages, S&L’s were granted permission to invest more aggressively, on the hopes that they would “outgrow their problems.” Unfortunately, this backfired and S&Ls made a lot of bad bets that only further compounded losses. By delaying the day of reckoning, it is estimated that the final cost to taxpayers of the S&L Crisis was six times greater than it could have been if it had been addressed earlier.

Source: Swan Global Investments

There are a lot of similarities between the current banking emergency and the situation from 40 years ago. A rapid rise in interest rates to squash inflation led to a devaluation of long-duration assets and a deposit flight amongst savings institutions; insolvency occurs.

To their credit, regulators are moving much more quickly to shut down problem banks or find buyers, unlike the situation 40 years ago. But we are still in the early stages of this emergency. It is unclear how many additional banks face similar problems as those already liquidated.

There are also many historical precedents that illustrate the “zombie bank” scenario. Japan in the 1990’s and early 2000’s is the most famous example. Following the boom years of the 1980’s, Japan was saddled with an unprofitable banking sector, unwilling to lend. This acted as an anchor on a stagnant economy; Japan faced not one but two “lost decades.” European banks in the 2010’s found themselves in a similar situation following the Global Financial Crisis and concerns about the Euro’s survival as a currency. China might also be a zombie bank candidate given the unresolved issues around their property market, but their situation is so opaque it is difficult for anyone to understand the true health of their financial system.

In each of these situations, the intentions were again good: to defer the pain and the admitting of losses in bad loans. But the consequences were an unproductive and inefficient deployment of capital and a drag on economic activity.

This unending cycle of well-intended-decisions-leading-to-disastrous-consequences can be supremely frustrating for clear-eyed investors. Those who approach investing with a skeptical or even a cynical outlook toward the policy decisions of politicians and regulators might feel helpless fighting against the tides released by such forces.

Swan Global Investments believes investors do have a choice: they can hedge their investments. Rather than stuffing their money under the mattress, they can invest in the market but maintain defensive positions in hedges, like put options, that should help mitigate losses when these negative consequences finally come home to roost.

Some consider hedging as a temporary solution—a tactical tool for times of potential distress. However, remaining always hedged may enable investors to mitigate market risk, which can at times materialize quickly. Our time-tested approach to actively managing long-term hedges around a portfolio of passively held equity ETFs may allow investors to remain invested into the strength of the broader market while maintaining a level of risk management. Hedging allows investors to remain invested and insulated from the consequences of others’ bad decisions.

Marc Odo, CFA®, FRM®, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 113-SGI-051023