Jan. 4, 2021

Insight Series – Comparing Hedging and Options Strategies

Strategy Comparison Series

With a covered call, the manager holds an underlying position on individual stocks or an index-like position. However, the manager seeks to supplement their return by systematically selling calls against their long positions and collecting that option premium. For more on a call option, see here.

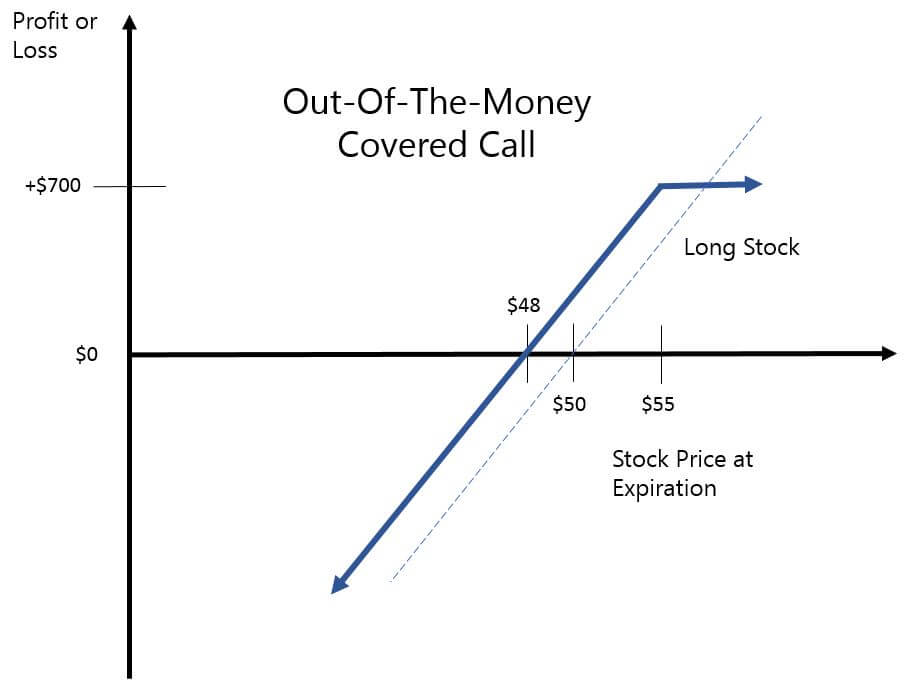

Below is a graph outlining the return profile of a covered call strategy, with the underlying stock as the dotted line and the combined equity-and-short-call return profile as the solid line.

Source: www.theoptionsguide.com

Seeking Portfolio Protection vs Portfolio Cushioning

Options strategies are increasingly becoming more accepted as a tool the portfolio construction. One of the most common option-based strategies is the covered call.

All options-based strategies are not created equal. However, many investors tend to lump all strategies that utilize options together. This is an erroneous approach, as different strategies have very different objectives and different ways of utilizing options.

With a covered call strategy the lion’s share of the holdings are in a buy-and-hold position in a stock or index. While the collection of option premium might supplement the returns, the primary driver of a covered call strategy will most likely be simply the upward or downward movement in the stock price.

While the covered call strategy sounds like a clever way to supplement return with income, there are two major risks associated with it: one on the upside and one on the downside.

The first risk is on the upside. If the markets take off too quickly, the call option goes in-the-money. Under such circumstances the portfolio manager really only has a few options:

Regardless, the covered call has effectively sold off its upside potential in a sharply rising market.

The other risk is on the downside. A covered call strategy offers no downside protection. The long position is unhedged and completely exposed to losses. The income from the sale of calls might offset a bit of the losses, but in a situation where the market sells off 20%, 30%, 40% or more, it is highly likely a covered call strategy would face similar losses.

Using a dated but still useful nomenclature, a covered call strategy essentially transforms a “growth” position (i.e., a long stock) to a “growth and income” play. The potential for larger gains is in effect swapped out for immediate income. In a low-yield world where dividend-paying stocks are trading at a premium, this type of approach might boost income if it works out.

The ideal scenario for a covered call strategy is a slowly rising market, where the equity position gains but never moves past the strike price of the call option. In such a situation the portfolio can collect income from the sale of calls, but not worry about having its market gains being sold away. Sadly, this situation doesn’t accurately describe much of what we’ve seen over the last decade or more. Either markets were selling off massively (2007-08) or rallying significantly (2009-10, 2012-2016). Neither situation is good for covered call strategies.

The Defined Risk Strategy (DRS) shares a few similarities with covered calls, in the sense that it has a core, buy-and-hold, long position and does sell options on that underlying long position. However, there are some key differences between the DRS and covered call strategies.

The DRS is better described as a hedged equity approach, where there is explicit downside protection on the equity in the form of a long-term LEAPS put option. There is a third component comprised of shorter-term options seeking premium collection, but the income is generated via the simultaneous sale of both calls and puts in a market-neutral fashion. All this leads to a very different return and risk profile than covered call managers.

The objective of this Strategy Comparison blog series is to help investors, and advisors, better understand these non-traditional strategies and how they compare and contrast to the DRS when making portfolio decisions.

See our previous posts on:

Looking for a deeper dive into portfolio strategies, check out our recently updated white paper on Optimizing Asset Allocation Strategies.

Our portfolio managers and analysts are dedicated to creating relevant, educational Articles, Podcasts, White Papers, Videos, and more.

Marc Odo, CFA®, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan Global Investments offers and manages the Defined Risk Strategy for investors including individuals, institutions and other investment advisor firms. All Swan products utilize the Swan DRS but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results and comparing results among the Swan products and composites may be of limited use. Indices are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. DRS results are from the Select Composite, net of fees, as of 12/31/2016. The charts and graphs contained herein should not serve as the sole determining factor for making investment decisions. Hypothetical performance analysis is not actual performance history. Actual results may materially vary and differ significantly from the suggested hypothetical analysis performance data. This analysis is not a guarantee or indication of future performance. Swan claims compliance with the Global Investment Performance Standards (GIPS®). Any historical numbers, awards and recognitions presented are based on the performance of a (GIPS®) composite, Swan’s DRS Select Composite, which includes nonqualified discretionary accounts invested in since inception, July 1997 and are net of fees and expenses. All data used herein; including the statistical information, verification and performance reports are available upon request.

The benchmarks used for the DRS Select Composite are the S&P 500 Index, which consists of approximately 500 large cap stocks often used as a proxy for the overall U.S. equity market, and a 60/40 blended composite, weighted 60% in the aforementioned S&P 500 Index and 40% in the Barclays US Aggregate Bond Index. The 60/40 is rebalanced monthly. The Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.

The advisor’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the advisor invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970.382.8901 or visit www.swanglobalinvestments.com. 061-SGI-030317