There are numerous risks working against treasuries, corporate, and high yield bonds that pose tremendous challenges to their traditional roles of income and capital preservation as well as their reputation of being safe investments.

With Treasury yields so low, some investors look to corporate bonds to fill their income and return needs. However, investors should be cautious of the credit and liquidity risks that have been building in the corporate bond market: low absolute yield, leverage, credit quality, and liquidity.

The amount of “take-home” income available to the investor from corporate bonds has been greatly reduced with the collapse in overall interest rates.

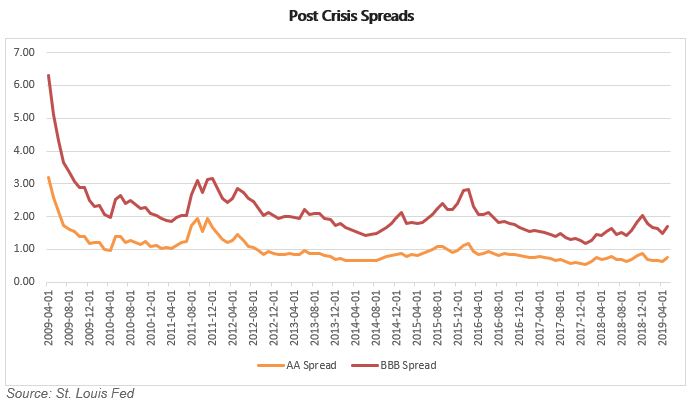

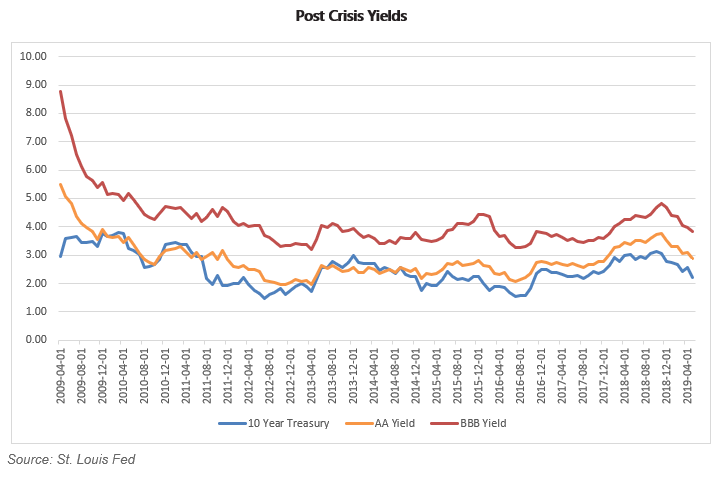

Corporate bonds are frequently valued on their spread over Treasuries. This is a relative measure of the compensation required for the credit risk above and beyond the baseline Treasury rate. In the decade since the Great Financial Crisis (GFC), spreads have fluctuated with market sentiment but have been range-bound. AA-rated corporate debt has typically sold at an average premium of 100 basis points to Treasuries, whereas the low-end BBB corporate debt’s spread has averaged 211 basis points.

However, there is an old saying in investing: “You can’t eat relative returns.” In absolute terms, the yield received from corporate issues is quite low.

The graph below illustrates the reality facing bond investors these last ten years. A 2% spread over Treasuries when Treasuries are yielding 6% leads to a respectable 8% in income.

Alternatively, a 2% spread over 2% Treasury yields amounts to an underwhelming 4% yield. For a retiree relying upon high quality Treasuries and investment grade corporate debt to pay the bills, their income is cut in half.

Another consequence of the liquidity flood was corporations becoming much more leveraged, and thus more susceptible to downturns in economic conditions.

With rates at historic lows, it was entirely rational for individual CFOs to restructure their firm’s existing debt or borrow more. Some say the whole point of the liquidity flood was to fuel the “animal spirits” of capitalism. Whether or not this led to productive use of capital or simply more share buy-backs benefitting existing equity shareholders is hotly debated.

What is not in question, however, is that corporations are more leveraged now than they were before the GFC. The overall size of U.S. corporate debt was around $9.2trn in late 2018, compared to $5.4trn in December 20071.

This leveraging up of corporate balance sheets has changed the composition of the corporate bond market.

An eye-opening point is that only two firms—Johnson & Johnson and Microsoft—are currently AAA rated by Standard and Poor’s. In contrast, there were 98 companies with the coveted AAA rating in 19922.

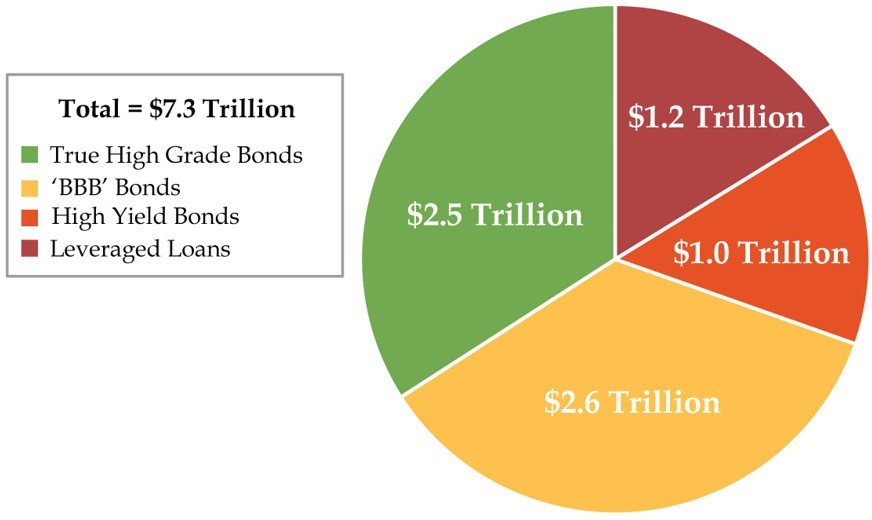

Moreover, in recent years the volume of debt on the lowest rung of the investment grade ladder has ballooned. There is currently over $2.5trn worth of BBB-rated debt, making up roughly half of the investment grade corporate bond pie. By way of reference, the entire investment grade corporate bond market was worth less than $1.75trn prior to the GFC in 20073.

Source: Quill Intelligence

Another consequence of the GFC was that many large banks dramatically reduced their inventory of corporate bonds. Banks used to play a market-maker type role for corporates, constantly buying and selling. With their mandated emphasis on higher-quality Treasury and Government issues, this role as a liquidity provider in corporate issues has been dramatically reduced in the last ten years.

It is estimated that in 2006 there was $200bn in corporate bonds in dealer inventory and that today the number is closer to $20bn—a reduction of 90%5. We have yet to see the liquidity of the corporate bond market severely tested since the banks have curtailed their participation in corporates.

It will also be interesting to see how quickly the rating agencies react to worsening conditions and downgrade issuers. Downgrades lead to forced selling and forced selling leads to liquidity problems.

In the aftermath of the GFC the rating agencies were heavily criticized for being too slow to respond to deteriorating economic conditions. Some claim the downgrades happened after it was too late for them to be useful to anyone. Whether or not this criticism compels the rating agencies to react and downgrade more quickly the next time a crisis hits will be closely watched.

Obviously, no one knows how the investment grade corporate bond market will respond to the next crisis until the moment it arrives. That being said, the current environment is much changed from what it was prior to 2007.

It’s prudent to assume investment grade corporate debt poses challenges to investors on two fronts: overall return potential and reduced ability to serve a capital preservation role during the next crisis.

With the low yields in corporate debt, many investors turn to high yield bonds. This is covered in the next post in the series.

Marc Odo, CFA®, CAIA®, CIPM®, CFP®, Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. Formerly, Marc was the Director of Research at Zephyr Associates for 11 years.

1 Securities Industry and Financial Markets Association.

2 “Triple A Quality Fades as Companies Embrace Debt.” The Financial Times; May 24, 2016

3 “The Corporate Bond Market is Getting Junkier.” Danielle DiMartino-Booth, Bloomberg; July 10, 2018

4 “Market Insight: The Storm Surrounding BBB-Rated Corporate Debt.” Tortoise Advisors, September 2018

5 “The Changing Nature of Market Liquidity- Understanding Banks’ Corporate Bond Inventory.” Richard Woolnough, Bond Vigilantes; April 4, 2019

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms. Any historical numbers, awards and recognitions presented are based on the performance of a (GIPS®) composite, Swan’s DRS Select Composite, which includes non-qualified discretionary accounts invested in since inception, July 1997, and are net of fees and expenses. Swan claims compliance with the Global Investment Performance Standards (GIPS®).

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. All investment strategies have the potential for profit or loss. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 395-SGI-101619